IV. Interest rates

The fresh new Government Houses Management provides all the FHA mortgages and claims new FHA-accepted financial in the eventuality of default, and therefore decreases the exposure towards bank when providing the mortgage.

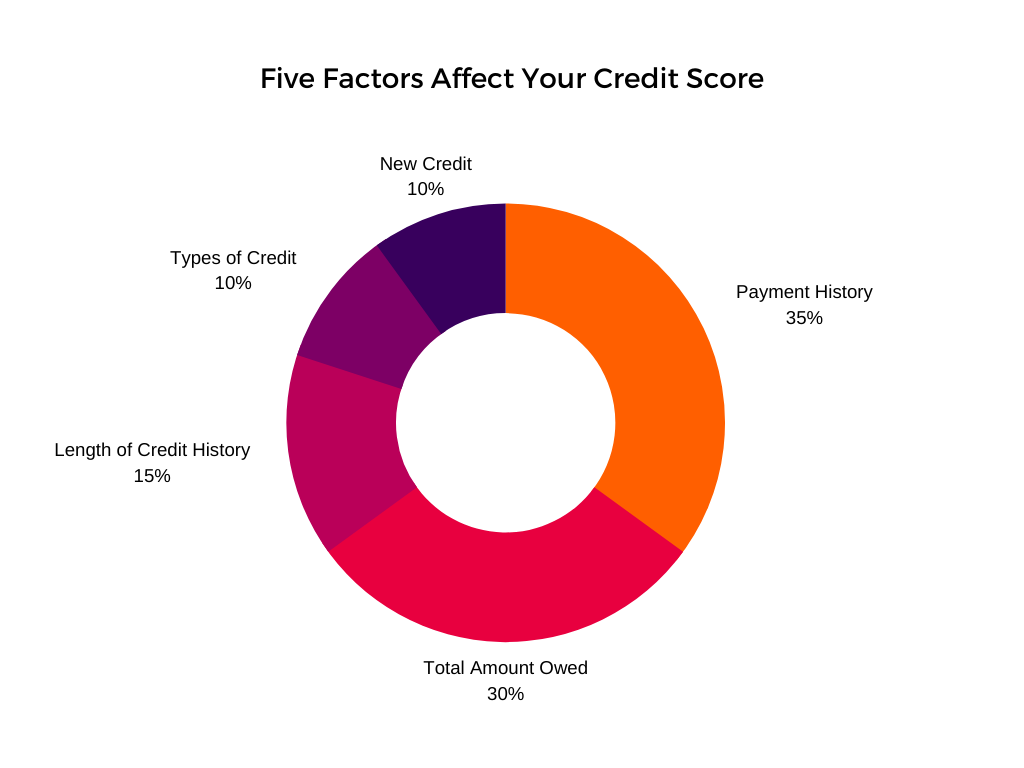

The interest rate to your an FHA mortgage otherwise antique mortgage is influenced by your credit score together with measurements of the down-payment. Other variables tend to be market conditions, mortgage method of (buy, cash-away re-finance), past financing repayment record, and you will whether or not you opt for a fixed-rate or a varying-speed mortgage.

FHA mortgage rates of interest basically be seemingly more desirable than simply conventional loans according to financing dimensions, downpayment, and property. They truly are FHA’s upfront and you may yearly financial cost (MIP).

V. Home loan Insurance coverage (MIP)

Really FHA mortgages have to have the percentage out of a mandatory Initial Financial Advanced (UFMIP) and annual Home loan Advanced (MIP), which covers the possibility of standard on your mortgage. The one-big date 1.75% UFMIP is non recoverable but into an enthusiastic FHA Streamline Re-finance.

A conventional mortgage need personal financial insurance (PMI) on condition that the newest down payment number try lower than 20% of one’s cost. It insurance is built to protect the financial institution if the mortgage standard. PMI pricing are based on your credit rating including the borrowed funds-to-value (LTV) proportion. PMI is often paid down due to the fact a fee every month. not, you I condition where in fact the financial pays the insurance, and you also spend a somewhat high interest to cover PMI.

PMI does be more expensive than the MIP towards the an enthusiastic FHA mortgage in the event the credit history try lower. not, in the event the credit score are 720 otherwise a lot more than, PMI can cost less than MIP. This will be a significant cost aspect to consider, FHA against old-fashioned financing.

VI. Mortgage Restrict

Restrict financing limitations apply to often solution, FHA compared to conventional mortgage. The latest Federal Homes Finance Service (FHFA) set the loan limitations into the conforming traditional funds, given that FHA set the borrowed funds restrictions to your FHA financing created to your geography. Low-prices parts are $420,860 and better pricing areas is $970,800.

The new FHFA manages Federal national mortgage association and you may Freddie Mac computer being authorities-sponsored businesses. Non-conforming old-fashioned money that aren’t supported by Fannie otherwise Freddie (known as Jumbo loans) lack constraints to the amount borrowed. Compliant traditional fund shouldn’t go beyond $647,200 (2022). In a few places, which limitation is generally large. For-instance, Fannie and you can Freddie ensure it is an amount borrowed up to $970,800 in some county areas.

VII. Property Criteria

With an enthusiastic FHA mortgage, the house or property may only be studied given that a primary house and you can shouldn’t be ordered in this 90 days of one’s prior selling. For traditional finance, the home may be used due to the fact a primary residence, second household, vacation domestic, otherwise investment property.

VIII. Bankruptcy

Case of bankruptcy cannot immediately disqualify you against often financing type of, FHA against old-fashioned financing. A borrower will get be eligible for an FHA loan 2 yrs shortly after a part eight case of bankruptcy release day. Having old-fashioned funds, the latest waiting months try couple of years on the discharge or dismissal big date to own a chapter seven personal bankruptcy.

To possess Section 13 bankruptcies, and therefore encompass a reorganization of one’s expenses, the brand new wishing months are number of years in the dismissal big date to have a normal loan.

IX. Refinancing

- What’s their refinancing mission? If you are searching to possess an earnings-out refi but i have a reduced credit score, after that an FHA refinance can be the best option.

- What is your existing mortgage? For individuals who actually have a keen FHA loan, after that an enthusiastic FHA Streamline Re-finance line funds don’t require money and you best way to apply for mba loans will borrowing confirmation or an appraisal (susceptible to eligibility criteria).